Monday, December 24, 2012

Denver Real Estate Gets Help From the Neighborhood Stabilization Plan

Denver Real Estate Investment Denver is going to get a boost from the recently announced 29.3 million Neighborhood Stabilization Program funding in 2010. There are high hopes that this stimulus plan will help the City of Denver's efforts to combat the foreclosures that have been a problem since the housing bust. This will not only improve Denver real estate, it will produce thousands of jobs for people involved in construction.

Log Cabins

Hortons portable buildings has been fully established for over 2 decades working throughout Redhill Surrey and the Uk. Hortons has a fantastic reputation for providing amazing quality timber building sectors, being able to manufacture and install any design of building. We have a standard range of Timber Buildings to choose from or we can manufacture to our customers specifications.

Sunday, November 18, 2012

Saturday, November 17, 2012

Real Estate Sales Collapse in Paris and Ile-de-France; New Home Starts Lowest Since 1998; VAT Hike to Make Matters Much Worse

Mainstream media offers little on the stunning collapse of real estate sales in France, notably Paris and Ile-de-France. Via Google translate, please consider Real Estate November 2012: figures for the month. Here are a few translate-unedited snips.

Hiking the VAT in face of falling demand is blazing stupidity. Apparently a VAT hike is an expectation rather than a done deal, but given other examples of stunning stupidity from France, including tax hikes and the Economically Insane Proposal: "Make Layoffs So Expensive For Companies That It's Not Worth It" one should expect no less from French president Francois Hollande.

For more examples of things about to wreck France, please consider "Google Law" Yet Another Warped Policy by Hollande; Government Motors French Style

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

2012 will remain a very bad year for real estate professionals. In this comprehensive figures on the property market in November 2012, discover the sharp decline in real estate sales in Paris and Ile-de-France.Blazing Stupidity

Even in Paris, it becomes difficult to sell a property

Notaries in Paris / Ile-de-France note that even in their region very attractive it becomes difficult to sell a property . Between June and August 2012, it has sold "only" 35,000 existing homes, or 19% compared to the same period in 2011.

Through the preliminary contracts, that is to say, the sales agreement signed but the sale is not yet final, notaries noted an accentuation of the decrease in sales in September 2012. To believe the figures MeilleursAgents which figure barometer advanced compared to the figures of notaries, there are currently -30 to -40% of sales in Paris and the Ile-de-France.

Borrowing rates are low, borrowers are scarce

The mortgage rates continue to fall slightly in November 2012 . That makes 8 months in a row that interest rates fall. Loans for short periods have the largest declines compared to last month.

On loans granted in October 2012, the average rate is 3.37% and the duration of payments is 207 months.

Despite these cheap rates, mortgage demand plunges more now. The Observatory Housing Credit CSA announces -45.8% in October 2012 compared to the same month of the previous year. This accentuates the fall of -30.5% of mortgages in the first 9 months of 2012.

Starts of new homes in the third quarter of 2012 recorded their lowest level since 1998

Only 66,932 new dwelling units have been started in the third quarter of 2012. This is the lowest level seen since the third quarter of 2012. This represents a decrease of 17.3% compared to the same period in 2011.

VAT at 10% instead of 7% for the building in 2014?

The maintenance and renovation of housing more than two years are subject to reduced VAT under certain conditions. After passage of the VAT rate in the building from 5.5% to 7% in 2012, the government expects an increase in the VAT rate to 10% through.

Hiking the VAT in face of falling demand is blazing stupidity. Apparently a VAT hike is an expectation rather than a done deal, but given other examples of stunning stupidity from France, including tax hikes and the Economically Insane Proposal: "Make Layoffs So Expensive For Companies That It's Not Worth It" one should expect no less from French president Francois Hollande.

For more examples of things about to wreck France, please consider "Google Law" Yet Another Warped Policy by Hollande; Government Motors French Style

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Lagarde Says Greece Deal Should be "Rooted in Reality"; Mish Says Lagarde Should be "Rooted in Reality"

Today's case of the "pot calling the kettle is black" comes from IMF chief Christine Lagarde in a warning to Brussels nannycrats and the ECB Greek deal should be "rooted in reality"

Objectives in Conflict

The problem for the IMF, Germany, the nannycrats in Brussels, ECB, and Greece is the "objective" of keeping Greece in the eurozone is one of the things destroying Greece.

It is wishful thinking that Greece is going to stay in the eurozone. I am all for a large dose of "reality" but the objectives of the Troika and the nannycrats in Brussels does not permit reality.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

An agreement among Greece's international creditors on reducing its large debt pile should be "rooted in reality and not in wishful thinking," the head of the International Monetary Fund said ahead of a tense meeting with European leaders.

"I am always trying to be constructive but I am driven by two objectives," she said in an interview, "to build and approve a program for Greece that is solid, that is convincing today, that will be sustainable tomorrow, that is rooted in reality and not in wishful thinking.

Objectives in Conflict

The problem for the IMF, Germany, the nannycrats in Brussels, ECB, and Greece is the "objective" of keeping Greece in the eurozone is one of the things destroying Greece.

It is wishful thinking that Greece is going to stay in the eurozone. I am all for a large dose of "reality" but the objectives of the Troika and the nannycrats in Brussels does not permit reality.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Friday, November 16, 2012

Fiscal Cliff Talks Underway Between Obama, House Speaker Boehner; Market Rallies on Talk of "Fluff" Compromise

The SP&P staged a mild (and meaningless) 19-point flagpole rally on news of a possible compromise between House Speaker John Boehner and president Obama as shown by the following chart of S&P Futures.

Market participants hope that Obama and Boehner agree to kick the can down the road. Most likely they will, the question is by how much.

Please consider Obama Opens Fiscal Cliff Talks as Boehner Open to Revenue

Read that last paragraph above carefully. No one in either party has the guts to stand up and say "we cannot afford this".

I talked about this earlier today in Ron Paul, American Hero; His Farewell Speech to Congress; Mish Reflections On Why the Country is Broke

Look for a compromise to do as little as possible to fix the structural problems in the US. Instead look for Republicans to scale back cuts in military spending and Democrats to scale back revenue increases.

The non-leaders in both parties will stand up and proclaim "we saved the US from the fiscal cliff" or some other self-congratulatory nonsense.

Once again, I am not in favor of tax hikes (unless they come at a steep price such as scrapping Davis-Bacon, ending collective bargaining of public unions, etc., things that will actually fix some structural problems).

However, I don't expect anything but fluff compromises because neither Obama nor Boehner has the courage to tell the truth.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Market participants hope that Obama and Boehner agree to kick the can down the road. Most likely they will, the question is by how much.

Please consider Obama Opens Fiscal Cliff Talks as Boehner Open to Revenue

House Speaker John Boehner said he offered a “framework” including new revenue to reduce the U.S. budget deficit in his first face-to-face talks today with President Barack Obama and top Congress leaders since the Nov. 6 election.Why the Country is Broke

As both sides expressed optimism that a deal is possible, U.S. equity markets rose.

Boehner also said he is serious about including revenue in an agreement if accompanied by significant spending cuts. The framework is “consistent with the president’s call for a fair and balanced approach,” he said after what he called a “constructive” meeting with the president and other congressional leaders in the Roosevelt Room at the White House.

“We’re prepared to put revenue on the table, provided we fix the real problems,” including entitlement costs, said Senate Republican leader Mitch McConnell of Kentucky.

Despite the optimism, the starting points for both sides -- Obama’s insistence on higher taxes for top earners and Republicans’ refusal to raise rates -- leaves negotiators with arithmetically complex and politically fraught choices.

While insisting on taxes, Obama has shown some openness in recent days. He and Geithner said rates must increase without specifying that the top rate must return to the 39.6 percent level in effect when President Bill Clinton left office.

Democrats and some Republicans are also beginning to talk publicly about another alternative: a more modest increase in upper-income tax rates.

One idea would be to raise Obama’s $250,000 income threshold for a tax increase to $500,000 or $1 million and increase the current 35 percent top rate to 37 percent, Peter Orszag, Obama’s former director of the Office of Management and Budget, said today on Bloomberg Television.

“Will John Boehner really blow up a deal for a 1 percent point increase above $1 million?” Orszag said. “The administration has made it clear there has to be at least some increase in marginal tax rates.”

Several congressional aides have suggested that in the event talks fail, both parties in Congress are discussing fallback plans for $60 billion to $100 billion in deficit reduction to replace automatic spending cuts set to take effect in January.

Read that last paragraph above carefully. No one in either party has the guts to stand up and say "we cannot afford this".

I talked about this earlier today in Ron Paul, American Hero; His Farewell Speech to Congress; Mish Reflections On Why the Country is Broke

Question of the DayExpect Fluff Compromise

If Republicans are not in favor of deficit spending and Democrats are not either, then how the Hell do we have trillion dollar deficits?

The answer is vast majority of politicians are liars, with no backbone to stand up and tell the truth to US citizens: "the country is broke".

We cannot afford wars. We cannot afford to keep troops in 140 countries. We cannot afford to be the world's policeman.

We also cannot afford Davis-Bacon and prevailing wage laws. We cannot afford the pension promises we have made. We cannot afford collective bargaining of public unions. We cannot afford all kinds of entitlements that have been promised.

How Does It Happen?

We have all of these things because corrupt politicians buy votes of constituents who want to hear the lie that we can afford those things. In the end, that's what it's really all about.

The unions, the warmongers, the banks, and all the other special interest groups buy votes of corrupt politicians every step of the way. The "compromise" in Congress is Republican get their wars and Democrats get fiscally unsound social programs.

Look for a compromise to do as little as possible to fix the structural problems in the US. Instead look for Republicans to scale back cuts in military spending and Democrats to scale back revenue increases.

The non-leaders in both parties will stand up and proclaim "we saved the US from the fiscal cliff" or some other self-congratulatory nonsense.

Once again, I am not in favor of tax hikes (unless they come at a steep price such as scrapping Davis-Bacon, ending collective bargaining of public unions, etc., things that will actually fix some structural problems).

However, I don't expect anything but fluff compromises because neither Obama nor Boehner has the courage to tell the truth.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Weak Regional Manufacturing Surveys: Philly Fed, NY Fed, Dallas Fed; Don't Blame Hurricane Sandy

Let's take a look at the latest Fed regional economic surveys to catch a glimpse at current business conditions.

Philly Region Back in Contraction

The November 2012 Philadelphia Business Outlook Survey is back in negative territory.

Current and Future Business Activity

Don't Blame Sandy

It's tough to pin this all on Hurricane Sandy although many will try.

New York Manufacturing in Contraction Fourth Month

The Federal Reserve Bank of New York Empire State Manufacturing Survey shows manufacturing declines at modest pace.

NY Fed Business Conditions

Expansion Slows in Dallas Region

The Dallas Fed Texas Manufacturing Survey shows manufacturing activity expands at a slower pace.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Philly Region Back in Contraction

The November 2012 Philadelphia Business Outlook Survey is back in negative territory.

Indicators Suggest Diminished Activity

The survey’s broadest measure of manufacturing conditions, the diffusion index of current activity, decreased 16 points, to a reading of ‑10.7. The fallback of the general activity index followed a single positive reading in October that was preceded by five negative monthly readings. Nearly 32 percent of firms reported declines in activity this month, while 21 percent reported increases. The demand for manufactured goods, as measured by the current new orders index, declined 4 points from last month and remains in negative territory. Shipments also fell this month: The current shipments index fell 7 points, to ‑6.7. Declines in inventories were also more widespread this month; 31 percent of firms reported declines compared with 21 percent in October.

Labor market conditions at the reporting firms remained weak this month. The current employment index, at ‑6.8, was slightly improved from its negative reading in October (‑10.7) but has remained negative for five consecutive months. The percentage of firms reporting decreases in employment (20 percent) exceeded the percentage reporting increases (13 percent). Firms also indicated fewer hours worked: The average workweek index was virtually unchanged but posted its eighth consecutive negative reading.

Current and Future Business Activity

Don't Blame Sandy

It's tough to pin this all on Hurricane Sandy although many will try.

New York Manufacturing in Contraction Fourth Month

The Federal Reserve Bank of New York Empire State Manufacturing Survey shows manufacturing declines at modest pace.

The November 2012 Empire State Manufacturing Survey indicates that conditions for New York manufacturers declined at a modest pace. The general business conditions index was negative for a fourth consecutive month, but was little changed at -5.2. The new orders index rose above zero for the first time since June, although it was only slightly positive at 3.1.

Labor market conditions were noticeably weaker. The index for number of employees

fell fourteen points to -14.6, a sharp drop to its lowest level since 2009, and the average workweek index drifted down to -7.9.

In a series of supplementary questions, firms were asked about the extent to which their businesses were affected by the “superstorm” Sandy. Among firms based in upstate New York, only 21 percent reported any loss of activity due to the storm—and in most cases, for no more than one day.

Business Conditions Decline Modestly

The general business conditions index was little changed in November and, at -5.2, suggested that activity for New York manufacturers continued to decline at a modest pace. Nineteen percent of respondents reported that conditions had improved over the past month, while 24 percent reported that conditions had worsened.

NY Fed Business Conditions

Expansion Slows in Dallas Region

The Dallas Fed Texas Manufacturing Survey shows manufacturing activity expands at a slower pace.

Texas factory activity increased in October, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, dipped from 10 to 7.9, indicating slightly slower growth.While not outright horrid, the regional manufacturing surveys show renewed weakness that is tough to pin on Hurricane Sandy. I expect conditions to deteriorate further.

Most other measures of current manufacturing activity also suggested growth in October, although new orders declined. The capacity utilization index edged up from 9.3 to 11.4, with more than one-quarter of manufacturers noting an increase. The shipments index held steady at 4.7, suggesting shipments rose at about the same pace as in September. The new orders index fell from 5.3 to –4.5, reaching its lowest level this year and indicating a decrease in demand.

Labor market indicators reflected slow but steady labor demand growth and shrinking workweeks. The employment index was 5.2 in October, largely unchanged from last month but well below the higher levels seen earlier in the year. About 15 percent of firms reported hiring new workers, while 10 percent reported layoffs. The hours worked index fell back into negative territory with a reading of –5.9, down from 2.8 in September.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Friday, November 2, 2012

5 million jobs and counting

The economy has generated about 5 million new jobs since early 2010. The pace of jobs growth has been disappointing, but it has been relatively steady. More importantly—since the market is still very fearful of another recession—there are no signs here of any emerging weakness. Private sector jobs growth is decent, but not strong enough to result in any meaningful decline in the unemployment rate, which remains high.

This chart shows the total number of jobs according to the Establishment and the Household Surveys. Both are showing a net gain of about 5 million jobs since early 2010. That works out to a little over 150,000 jobs per month on average.

This chart of the labor force (those who are working plus those who are looking for work) shows that it tends to grow about 1% per year. One salient feature of the current recovery is the lack of growth in the labor force—the result of approximately 7 million people apparently deciding to "give up" looking for a job. However, in the past year the labor force has resumed its trend growth rate of 1% per year and has reached a new high. On the margin this is a modest positive, since it reflects increased optimism and a more dynamic workforce.

If the 7 million people who have given up looking for work should decide to get back in the hunt, the unemployment rate would jump to something like 12%. Most of the decline in the unemployment rate during this recovery is due to the unprecedented number of people who have dropped out of the labor force.

This chart shows only private sector employment, by excluding the 20-22 million people who are employed by various levels of the public sector. Note how much more volatile the household survey is. On average, both surveys are saying the same thing, and they are consistent with an economy that is growing at a 2-3% pace. That growth rate can be decomposed into 1.5-2% jobs growth and 1% productivity growth. Nothing to write home about, but neither is it something to disparage.

This chart compares private sector to public sector jobs. This recovery has seen a substantial decline in public sector jobs (about 600K), but the declining trend appears to have stalled. Public sector jobs are flat year to date. This suggests that state and local governments have managed to bring their expenses more into line with their revenues, and that is another positive change on the margin.

Thursday, November 1, 2012

Construction spending still weak, but improving

Construction spending in September was up 0.6%, and in line with expectations. As these charts show, construction spending on both nonresidential and residential structures is up 14% from last year's low. After years of a disastrous decline, construction is now expanding faster than the overall economy. The sector is still very weak, but on the margin things are getting better.

Layoff activity remains relatively low

New claims for unemployment have been relatively flat this year, down about 8% or so from year-ago levels. This is consistent with continued, albeit sluggish, economic growth. The Challenger tally of announced corporate layoffs (second chart above) tells a similar story. Nothing much happening here, but at least there's no sign of any deterioration in the economy.

If there is one bright spot in the labor market, it is the ongoing decline in the number of persons receiving unemployment insurance: 20% fewer people today (1.3 million) are receiving unemployment checks than were a year ago. This motivates people to find and accept a new job, even one paying less than they would have liked. In a slow-growing economy, this is unfortunately the only way that excess labor can be absorbed: the price of labor has to decline. Extended unemployment insurance payments only serve to slow that process.

ADP employment report only modestly positive

ADP has revised its methodology, and this appears to have improved the ability of its estimate of private sector jobs growth to predict the BLS establishment survey of jobs growth. This suggests that tomorrow's private sector jobs number could be modestly higher than expected (158K vs. 124K).

The first chart above is from last month (September data), before ADP changed its reporting and forecasting methodology. The second chart uses the new and revised data through October. To my eye, the new ADP series more closely tracks the BLS data, especially in the past year or so. If this holds up, then it means that tomorrow's jobs report should be somewhat better than expected. Even so, jobs growth of 160K is only enough to absorb new entrants to the labor market, and far short of what it would take to bring about a meaningful reduction in the unemployment rate. So I wouldn't expect another decline in the unemployment rate, and I note that expectations call for it to rise from last month's 7.8% to 7.9%.

The outlook for economic growth remains uninspiring, but the good news is that there is no sign of deterioration. But since the market remains braced for bad news, this dull news ends up being good news.

The first chart above is from last month (September data), before ADP changed its reporting and forecasting methodology. The second chart uses the new and revised data through October. To my eye, the new ADP series more closely tracks the BLS data, especially in the past year or so. If this holds up, then it means that tomorrow's jobs report should be somewhat better than expected. Even so, jobs growth of 160K is only enough to absorb new entrants to the labor market, and far short of what it would take to bring about a meaningful reduction in the unemployment rate. So I wouldn't expect another decline in the unemployment rate, and I note that expectations call for it to rise from last month's 7.8% to 7.9%.

The outlook for economic growth remains uninspiring, but the good news is that there is no sign of deterioration. But since the market remains braced for bad news, this dull news ends up being good news.

Manufacturing doesn't deteriorate, and that is the good news

The ISM manufacturing report came in slightly better than expectations, but remains lackluster.

As the chart above suggests, the ISM manufacturing index is consistent with real GDP growth of 2 or maybe 3%. It's steady as she goes, and she isn't going very fast. Nothing new to see here.

Export orders continue to show some weakness, which is not surprising given the struggles in the Eurozone and the slowdown in China that have been widely remarked. Still, the recent readings are not weak enough to point to any serious problems, and the latest news from China—where the purchasing managers' index has been around 50 for the past several months—suggests that the slowdown has not worsened.

The prices paid index points to mild inflation pressures, nothing unusual.

The employment index has been only mildly positive for the past year. This suggests that manufacturing is not likely to pick up meaningfully nor deteriorate in coming months.

Add it all up, and it looks like the producers and risk-takers of the world have pulled in their horns in an attempt to brace for the uncertainty of the looming fiscal cliff. As a supply-sider I strongly reject the notion that the problem we have today is one of insufficient demand. On the contrary, the problem is insufficient "supply:" a dearth of new investment, risk-taking and work. Those are the things that create new jobs, and new jobs are the things that result in increased demand.

These facts do not paint a rosy picture of the future, but neither do they point to any meaningful deterioration on the margin. And that is the good news, since the market remains braced for bad news. 10-yr Treasury yields of 1.7% only make sense in a world where markets hold out very little hope for meaningful growth and indeed fear that another recession is practically unavoidable. As long as the economy avoids a recession, risk assets are going to continue to rise, albeit slowly.

Monday, October 29, 2012

Inflation, deflation, and the iPad mini

The debate over inflation—which ranges all the way from those who see the imminent risk of deflation to those who see hyperinflation just around the corner—continues, and with good reason. Inflation is alive and well in the services and nondurable sectors of the economy, while deflation is the "new normal" in the durable sector of the economy. Some prices are going up, but others are going down; on average, the government is telling us that inflation is only about 2%. That's a calm surface on a body of water that is roiling underneath.

The first of these two charts shows the average price level for each major sector. Service sector prices have risen about 60% over the past 18 years, while the price of nondurables are up a little over 50%. But durable goods prices have fallen steadily, and are now down a total of 28%. In the entire history of these series, there has never been a sustained period of declining prices except for the past 18 years in the durables sector. Not coincidentally, that period corresponds to the emergence of China as a powerhouse producer of durable goods (e.g., computers and TVs). Memo to Romney and Obama: China has done us a great service by producing products so cheaply.

If we make the assumption that the price of services is a proxy for wages and salaries, then what we see here is arguably the most incredible increase in workers' purchasing power in the history of the world. Do the math: over the past 18 years, services are up 161% and durables are down 28%. 161/.72 = 223.9. Salaries have more than doubled relative to durable goods. Put another way, an hours' worth of work now buys more than twice as much in the way of durable goods as it did 18 years ago—it takes 55% less work today to buy the typical durable good than it did 18 years ago. Bottom line, labor has become a whole lot more valuable and more expensive than things, especially very sophisticated and powerful things like computers.

Which leaves me puzzled as to the brouhaha over whether the iPad mini—the newest durable good to be offered to the public—is a whole lot more expensive, at a price of $329, than the Amazon Kindle Fire HD at $199. As the link demonstrates, there are some significant differences in features between the two devices. My point is whether the price of those differences—$130—is a huge amount. Is a 35% larger screen + a 5 mp camera + greater video compatibility + hundreds of thousands of extra apps + aluminum construction (vs. plastic) worth an extra $130? Consider what $130 gets you these days: a dinner for two with a bottle of wine at an upscale restaurant; a pair of jeans at Nordstrom; two tanks of gasoline; admission for one to Disneyland; a bottle of Dom Perignon; a small basket of groceries.

The average person now has available to him or her gadgets that 18 years ago would have been considered magical, if not impossible. With only one week's worth of minimum wages in California ($8/hr), you can buy yourself an iPad mini: a device that connects you to all information in the world; that holds and displays and edits and takes thousands of videos and photos; that holds your entire music library; that lets you read millions of books; that holds and displays maps of the entire world; that lets you explore the cosmos by simply pointing at the stars at night; that lets you read hundreds of newspapers; that lets you plan and reserve flights and hotels all over the world for free; that let's you play and record all kinds of music; that gives you access to thousands of video games that never before existed; that let's you correspond with people instantly all over the world; that's lets you fly dozens of planes realistically. I could go on, but I hope my point is clear. 18 years ago a device like the iPad mini would have been inconceivable no matter how much it cost. Today, in contrast, we are quibbling about whether such a device should cost $200, $250 or $330, when the difference is almost insignificant for the vast majority of people.

It is undeniably deflationary when a week's worth of work at minimum wage buys you things that only 18 years ago would have been unavailable to even the richest person on the planet. But at the same time, it costs an employer 2.2 times as much to hire that minimum wage worker, and it costs us all 5 times more to fill our tanks with gasoline. That's a lot of inflation. Or is it?

No wonder the debate rages.

Friday, October 26, 2012

Money demand continues to rise

We know this has been a miserable recovery—arguably the weakest ever—but exactly why is still a question that has not been answered to everyone's satisfaction. What follows is an attempt at a technical explanation based on the growth of the money supply and the nominal economy.

As the first of these two charts show, the M2 measure of money supply has grown at a fairly steady pace of about 6% per year for the past 17 years. As the second chart shows, the pace has picked up a bit since the Eurozone panic of last summer: since May '11, M2 is up at a 8.5% annualized pace. If all you knew were these two charts, you would guess that whatever has happened to the economy since the onset of the Great Recession hasn't involved any shortage of money.

As the first of these two charts show, the M2 measure of money supply has grown at a fairly steady pace of about 6% per year for the past 17 years. As the second chart shows, the pace has picked up a bit since the Eurozone panic of last summer: since May '11, M2 is up at a 8.5% annualized pace. If all you knew were these two charts, you would guess that whatever has happened to the economy since the onset of the Great Recession hasn't involved any shortage of money.

Of course we all know that the Fed has been trying very hard to inject money into the economy for the past four years, and they have achieved a measure of success: since Sept. '08, the M2 money supply is up $2.2 billion, with $300 billion of that coming from additional currency in circulation and the rest from an increase in bank savings deposits. Banks now hold $6.5 trillion of savings deposits, and that represents almost two-thirds of M2. But so far, all this extra money hasn't had much impact on either the economy or inflation. The economy has only managed a bit more than 2% growth over the past three years, and inflation has only been about 2%; nominal GDP is growing only 4%, far less than the 8.3% annualized pace of the past 30 years.

What's happened to all the money is that almost $1 trillion of the money that the Fed has succeeded in injecting into the economy over the past several years hasn't actually gone anywhere. People are holding on to it in bank savings accounts, and the banks in turn have invested the money in bank reserves that are sitting on the Fed's balance sheet. Most of the bank reserves that the Fed created to purchase notes and bonds have been willingly held by cautious savers and banks. The Fed has succeeded mainly in swapping bank reserves—essentially equivalent to T-bills since they pay about the same amount of interest and have an implicit government guarantee—for notes and bonds.

As the chart above shows, there has been a huge increase in the world's demand for M2 money (M2 growth has been much faster than nominal GDP growth). Like corporations that are reluctant to reinvest their profits (which are at record levels in terms of GDP), individuals are reluctant to spend the money they have instead been stashing in their savings accounts. (For more detail, see my series on The Reluctant Recovery starting here.) Everyone wants to be more conservative, pay down debt, and build up their cash reserves. Why? Because there are too many uncertainties looming: the fiscal cliff, the trillion dollar deficits that portend a huge increase in tax burdens, the regulatory uncertainties created by things like ObamaCare, the Eurozone sovereign debt crisis, and the Fed's massive balance sheet expansion which could theoretically ignite a huge burst of inflation, to name just a few.

If money demand keeps increasing, then the Fed will not be able to achieve much in the way of real or nominal GDP growth. What's needed is a change in the fiscal policy outlook, more than anything. But if confidence in the future increases (or the uncertainties about the future lessen), then the demand for M2 would likely begin to decline, and there could therefore be a tidal wave of liquidity attempting to exit bank savings accounts in order to relocate in nominal GDP. In addition to that, we have the possibility that banks might decide to use some or all of their current $1.4 trillion of excess reserves in order to expand their lending activities. Either way there is enough money in the system to boost nominal GDP significantly in the years to come, if conditions are ripe. How and when that might happen is still uncertain, as is the issue of how much of the additional nominal GDP would would be attributable to real growth.

But that is the essence of the problem today: there are some huge uncertainties out there, and that has simply dampened the animal spirits of nearly everyone. The November elections have the potential to create a great deal of change on the margin.

Quick thoughts on GDP: more stagflation

Third quarter real GDP growth was a bit stronger than expected (2.0% vs. 1.8%), but to me that was not the big news of the day. The more significant "beat" in the data was the GDP deflator, which came in at 2.9% vs. expectations of 2.1%. The combination of the two pushed nominal growth (on a quarterly annualized basis) up from 2.8% in the second quarter to 5.0% in the third quarter. With the exception of only 3 of the 13 quarters since the recovery began, nominal GDP growth has been 4% or better. We are a long way from facing any threat of deflation, and it should be abundantly clear that there is no shortage of money.

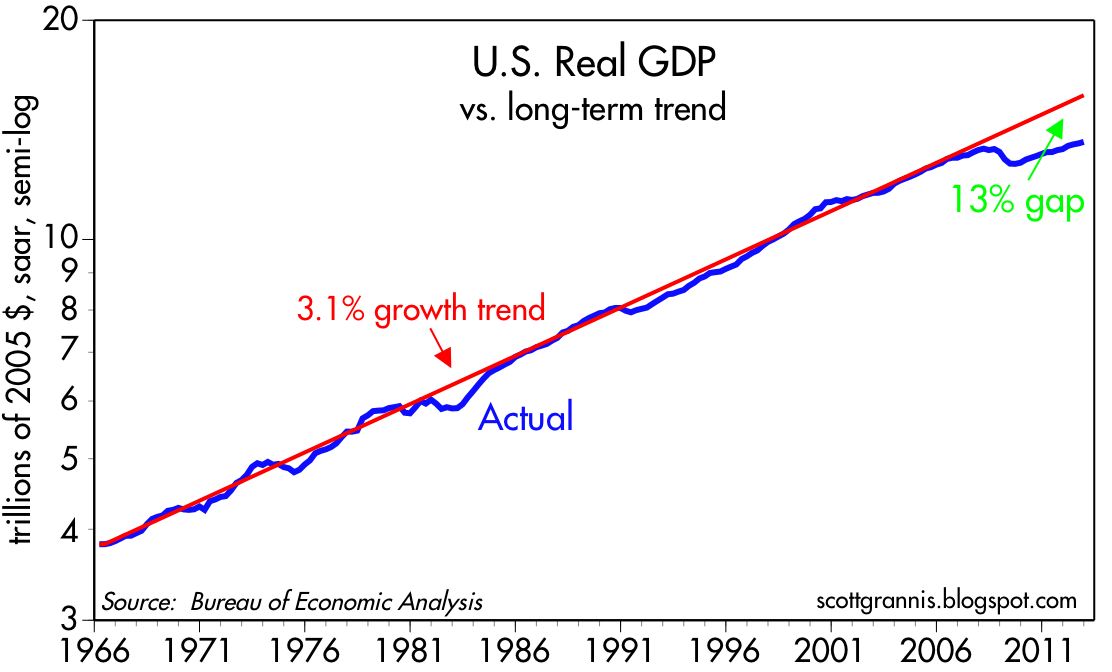

From a long-term perspective, this continues to be the weakest recovery ever. As the chart above suggests, the economy is about 13% smaller than it could have been absent the deep recession and the very meager recovery. That is equivalent to a little over $2 trillion of national income that has gone missing, and that accounts for at least half the size of the current federal deficit. In other words, the tax base on which current tax rates are applied is a lot smaller than it could have been.

The chart above shows the quarterly annualized rate of inflation according to the GDP deflator. The economy flirted only briefly with inflation late last year and in the second quarter of 2009, but other than that it looks like inflation is on track to be 2-3% going forward. This casts further doubt on the Fed's commitment to keep inflation low, since currently they are pursuing an obviously reflationary strategy at a time when inflation is at or above their target. It's not difficult to conclude that they are giving much greater weight to their full employment target at the expense of their inflation target.

This new inflation reality also clashes head-on with the yields on Treasuries. 5-yr yields are a measly 0.8%, 10-yr yields are a paltry 1.8%, and 30-yr yields are 2.9%. Negative real yields on everything out to 10 years mean that savers are being cheated and borrowers and speculators are being rewarded. The incentive to save is low and the incentive to speculate is high, and that is not a prescription for healthy economic growth. Erratic and inflationary monetary policy thus gets some of the blame for the slow growth of recent years. I worry that if the Fed keeps short-term rates close to zero for the next few years, as they promise, we could face a serious inflation problem in the next 3-5 years.

Thursday, October 25, 2012

Romney's wrong on China

I've said it before, and I'll say it again: Romney is dead wrong when he criticizes China for allegedly selling us stuff at a discount. Mark Perry does an excellent job explaining why we should be thrilled if indeed China is selling us stuff at artificially low prices. But as I explained last summer, there is no reason to think that China is undervaluing its currency in the first place.

This is such an important issue that it bears repeating. I've updated some charts to make my point clear.

By pegging the yuan to the dollar, China effectively outsourced its monetary policy to the Federal Reserve. On the surface, both countries have the same monetary policy, so both should have the same inflation rate, and that is indeed what has happened, as the chart above shows. China has been living under a US-influenced monetary regime for almost 20 years now, and its economy has had plenty of time to adjust. If the yuan were still undervalued, as Romney and even Obama claim, then Chinese inflation should be higher than US inflation, but it's not.

Anecdotal evidence suggests that on the margin more companies are finding it cheaper to produce goods in the US than in China, and that's part of the reason for the stability of China's reserves over the past year. It all adds up to evidence of a sort of equilibrium having been attained between the value of the yuan, the relative price levels in China and the US. The yuan has successfully compensated for the different level of productivity and specialization in each country.

There is nothing here to worry about, with one big exception: if the US tries to start a trade war with China to force it to revalue its currency even more, then we are all going to be in big trouble. The US could suffer from rising inflation (demanding a stronger yuan is equivalent to wanting a weaker dollar), while the Chinese could suffer from deflation. It's the politicians, not the Chinese, that pose the biggest threat to the US economy.

This is such an important issue that it bears repeating. I've updated some charts to make my point clear.

As the chart above shows, the Chinese yuan has been rising against the dollar ever since 1994. The Chinese are demonstrably not undervaluing their currency, they are continuous revaluing it. They have been forced to do this because of the tremendous inflow of capital to the country, which in turn has been driven by the world's desire to invest in this rapidly growing and dynamic economy. Since China's monetary policy is geared towards pegging its currency against the dollar, a net inflow of dollars and other currencies to the country obliges the central bank to buy the extra currency, thus adding to its forex reserves and expanding its monetary base. This is the way that capital inflows get turned into yuan and help the economy grow. But as the chart also shows, forex reserves swelled to over $3 trillion by last year, way more than enough to credibly back China's currency and its money supply.

For the past year, there has been no net addition to China's reserves, which means that there is no longer a net inflow of capital to China. This could be one sign that the currency is properly valued, and/or it could be a sign of a diminished desire on the part of foreigners to invest in China, and/or diminished investment opportunities in China, and/or a greater desire on the part of Chinese to invest abroad. Whatever the case, the central bank is no longer buying foreign currency to keep the yuan from rising, but they are still allowing the yuan to appreciate. This is not the behavior you would expect from a currency manipulator. If anything, the Chinese seem to be "manipulating" their currency higher against the dollar, not lower. And they might be doing this in order to proactively deflect criticism from misinformed and misguided politicians in the US.

This next chart shows the real value of the yuan against a large basket of currencies, as calculated by the BIS. Since it was first pegged to the dollar in 1994, the yuan has appreciated in real terms by 64%! Even supposing the yuan was purposefully undervalued in 1994, it is hard to believe that it is still undervalued today.

By pegging the yuan to the dollar, China effectively outsourced its monetary policy to the Federal Reserve. On the surface, both countries have the same monetary policy, so both should have the same inflation rate, and that is indeed what has happened, as the chart above shows. China has been living under a US-influenced monetary regime for almost 20 years now, and its economy has had plenty of time to adjust. If the yuan were still undervalued, as Romney and even Obama claim, then Chinese inflation should be higher than US inflation, but it's not.

Anecdotal evidence suggests that on the margin more companies are finding it cheaper to produce goods in the US than in China, and that's part of the reason for the stability of China's reserves over the past year. It all adds up to evidence of a sort of equilibrium having been attained between the value of the yuan, the relative price levels in China and the US. The yuan has successfully compensated for the different level of productivity and specialization in each country.

There is nothing here to worry about, with one big exception: if the US tries to start a trade war with China to force it to revalue its currency even more, then we are all going to be in big trouble. The US could suffer from rising inflation (demanding a stronger yuan is equivalent to wanting a weaker dollar), while the Chinese could suffer from deflation. It's the politicians, not the Chinese, that pose the biggest threat to the US economy.

Big changes in the labor market

The weekly unemployment claims data is among the most timely indicators available to track the economy's progress, which is why I post on this subject almost every week. In fact, the only thing timelier is market-based data, which is real-time.

Claims last week came in as expected, and they were almost identical to the average so far this year (370K vs. 369K). So there hasn't been much change this year in the underlying health of the jobs market, according to this measure.

But there has been a great deal of change, to judge by the 2.4 million decline in the nulber of people receiving unemployment compensation year to date. There are still an unusually large number of people receiving unemployment insurance given that we are three years into a recovery, but at least the number is declining steadily: it's down over 20% in the past 12 months, and down by one-third so far this year.

The chart above shows how different this recession has been from other recent recessions: at the peak, the percentage of the labor force receiving unemployment compensation was 67% more than at the peak of the 1981-82 recession. This goes a long way to explaining why this recovery has been so tepid. It's been the weakest recovery ever, in part because we've never paid so many people for so long not to work. And the main cause of that huge increase was Congress' decision in July 2008 to create a program called "Emergency Claims," which went on to double the number of people receiving benefits by early 2010. Congress' "compassion" for the unemployed had the unintended consequence of slowing and drawing out the recovery for everyone.

These charts document the single biggest change on the margin that is happening to the U.S. economy these days. Fortunately, it is a positive change on the margin, since it results in increased incentives to find and accept a new job, even if it doesn't pay very much. In the end, the only way a true recovery can take place is if unwanted labor is able to relocate and reprice itself so as to be attractive to new employers. That process is clearly underway, and it is one very good reason why the economy should continue to grow.

Wednesday, October 24, 2012

The Reluctant Recovery: Conclusions

This is the title of a presentation I gave October 10th to The Economic Club of Sheboygan. This post discusses the investment implications of the presentation. This is the fifth and final part in a series (see Part 1 here, Part 2 here, Part 3 here, and Part 4 here).

If there is one unifying theme to my presentation, it starts with the title. I argue that the recovery has been a reluctant one, because the market has from the very beginning been reluctant to embrace the notion that the recovery was real and durable, much less robust. There are plenty of good reasons for the market to be concerned, of course: unprecedented changes in monetary policy, misguided fiscal stimulus, the deep-seated problems in the Eurozone, the housing disaster, and the huge federal deficit, among others.

In Part 1, I show how key market-based indicators reflect a significant improvement in economic and financial fundamentals (e.g., swap spreads, real short-term hnterest rates, the slope of the yield curve, corporate profits), but other indicators show that the market remains very pessimistic about the future (e.g., TIPS yields, credit spreads, PE ratios, equity yields). The fundamentals have improved, but market sentiment remains pessimistic. This creates an interesting environment for investors, since it means that the bar for economic performance has been set very low: the economy only needs to avoid a recession for markets to react positively.

In Part 2, I argue that monetary policy has correctly responded to a huge increase in the demand for safe-haven dollar liquidity that followed in the wake of the Great Recession. But since the Fed's response was not only unprecedented but gigantic by historical standards, this has created tremendous uncertainty. Will the Fed be able to reverse its Quantitative Easing in a timely fashion? Should we be bracing for a significant increase in inflation? Will the dollar, already very near its weakest level ever, go down further?

In Part 3, I point out that although the federal budget is in miserable shape, there have been encouraging signs of progress. Spending as a % of GDP has declined, thanks to Congressional gridlock. Revenues as a % of GDP have increased, thanks to slow but steady growth in jobs and incomes. As a result, the budget deficit has dropped from a threatening 10.5% of GDP to now only 7%. This points to a relatively simple solution for the future: maintain spending restraint, avoid increasing tax rates, reduce tax rates as much as possible, and pay for lower rates by broadening the tax base (e.g., eliminating or limitation tax deductions and loopholes). In other words, there is a growth-oriented solution to our fiscal problem that needn't be difficult to implement.

In Part 4, I find that although this is the weakest recovery ever, there are a number of areas in the economy that are improving, and only a few that point to further weakness. Households have undergone tremendous deleveraging, and are much more financially healthy than before. Corporations have cut costs to the bone and are now more profitable than ever. The housing market is turning up. Banks are lending more. The main obstacles to progress are the uncertainty created by misguided fiscal policy, unprecedented monetary policy, and the looming fiscal cliff.

So, the market has dreadful expectations for the economy, but the economy is displaying many classic signs of an ongoing recovery, albeit a very tepid and disappointing one. The bar of expectations has been set very low. If the economy avoids a recession and continues to recover, even very slowly, this likely would be a positive shock to the market. Investors willing to bet that we do in fact avoid a recession can therefore expect to profit by buying risk assets that are relatively cheap by historical standards.

What follows are general guidelines for investing in different asset classes.

Equities are relatively cheap, in my view, because corporate profits are very high, both nominally and relative to GDP, but PE ratios are below average. Moreover, equity yields are significantly higher than corporate bond yields (the earnings yield on the S&P 500 is currently about 7% vs. a yield of 4.5% on the average BAA-rated corporate bond), and both are orders of magnitude higher than the yield on cash, which is another way of seeing that the market expects profits to decline significantly. If profits merely stagnate, equity yields would still be very attractive compared to corporate bond yields and unbelievably attractive relative to cash. It might take an outright recession or worse to shock the equity market.

Real estate, particularly residential real estate, has fallen significantly in price, while at the same time the cost of buying real estate using extremely low mortgage rates is very cheap—historically cheap—relative to household incomes. In other words, the affordability of housing has almost never been so attractive. That's because the majority of people still expect real estate prices to decline, despite growing signs of a housing market recovery and rising prices. It's also likely that demand for housing is being suppressed because banks' lending standards are still much tougher than they were before the Great Recession. Undoubtedly there are many young homeowners who would like to buy a house but find that they lack the necessary down payment or job history. Nevertheless, "everyone knows" that there is a ton of foreclosed properties sitting on banks' balance sheets waiting to be sold, and there are millions of homeowners still underwater on their mortgages. The real estate market is still in the grips of caution, rather than exuberance.

Real estate is also potentially very attractive because it has traditionally been an excellent inflation hedge. If the Fed fails to reverse its Quantitative Easing in a timely fashion, inflation could rise significantly. Incomes would also rise in that case, and the demand for housing could rise hugely. We all learned in the 1970s that real estate (and any hard asset, for that matter) is a great thing to own, especially with leverage, when inflation is rising. Today, however, both real estate and mortgage rates are priced to the expectation that inflation will remain relatively low for as far as the eye can see.

What about other inflation hedges? Gold prices are extremely high, both in nominal and real terms, and commodity prices have risen substantially. These markets arguably are priced (by speculators) to the expectation that the Fed will make a big inflationary mistake. Maybe they will, but if they don't, gold in particular could tumble much as it did in the 1980s when tight monetary policy caused inflation to fall way below everyone's expectations. It's late in the game to load up on gold, because the world has been loading up on gold for the past decade, in the expectation that inflation will rise, the dollar will collapse, and/or the global financial system will collapse. Barring any of these disasters, gold might have very limited upside but a lot of downside potential.

Treasury yields, meanwhile, are extraordinarily low, making Treasury bills, notes and bonds extraoridinarily expensive. Investors everywhere are willing to hold Treasuries at historically low levels of yield because they are very fearful of the future. With real yields on TIPS deep in negative territory, this is one more sign that expectations for future investment returns, and for real economic growth, are dismal. Thus, holding Treasuries today only makes sense if you worry about an outright depression. If the economy picks up even just a little, and/or inflation rises by even a few percentage points, Treasury yields could rise (and their prices fall) by enough to wipe out many years' worth of income.

Corporate and emerging market debt have performed very well in the past several years, because spreads to Treasuries have narrowed from very high levels and default rates have fallen thanks to an improving economy. Investment grade spreads are still somewhat wide by historic standards, but their yields have never been so low (3-3.5% currently). High quality corporate bonds still offer yields that are a few points higher than Treasuries, but if Treasury yields rise, investment grade corporate debt is going to face challenging conditions (i.e., rising yields and falling prices). In other words, current yields offer very little protection from a rising interest rate environment should the economy improve. High-yield corporate bonds offer more protection against rising yields, since their spreads to Treasuries are still relatively generous and their yields are in the range of 6-7%, but high-yield debt is no longer the slam-dunk it used to be. The current appeal of high-yield debt is that if nothing changes it offers much higher yields than Treasuries, and if yields rise, then the negative impact of rising yields would likely be offset to some degree by declining default rates and by declining spreads to Treasuries. That's because higher yields would only occur if the economy improves and/or inflation rises, and both of those conditions would make high-yield debt more attractive.

So, the market has dreadful expectations for the economy, but the economy is displaying many classic signs of an ongoing recovery, albeit a very tepid and disappointing one. The bar of expectations has been set very low. If the economy avoids a recession and continues to recover, even very slowly, this likely would be a positive shock to the market. Investors willing to bet that we do in fact avoid a recession can therefore expect to profit by buying risk assets that are relatively cheap by historical standards.

What follows are general guidelines for investing in different asset classes.

Equities are relatively cheap, in my view, because corporate profits are very high, both nominally and relative to GDP, but PE ratios are below average. Moreover, equity yields are significantly higher than corporate bond yields (the earnings yield on the S&P 500 is currently about 7% vs. a yield of 4.5% on the average BAA-rated corporate bond), and both are orders of magnitude higher than the yield on cash, which is another way of seeing that the market expects profits to decline significantly. If profits merely stagnate, equity yields would still be very attractive compared to corporate bond yields and unbelievably attractive relative to cash. It might take an outright recession or worse to shock the equity market.

Real estate, particularly residential real estate, has fallen significantly in price, while at the same time the cost of buying real estate using extremely low mortgage rates is very cheap—historically cheap—relative to household incomes. In other words, the affordability of housing has almost never been so attractive. That's because the majority of people still expect real estate prices to decline, despite growing signs of a housing market recovery and rising prices. It's also likely that demand for housing is being suppressed because banks' lending standards are still much tougher than they were before the Great Recession. Undoubtedly there are many young homeowners who would like to buy a house but find that they lack the necessary down payment or job history. Nevertheless, "everyone knows" that there is a ton of foreclosed properties sitting on banks' balance sheets waiting to be sold, and there are millions of homeowners still underwater on their mortgages. The real estate market is still in the grips of caution, rather than exuberance.

Real estate is also potentially very attractive because it has traditionally been an excellent inflation hedge. If the Fed fails to reverse its Quantitative Easing in a timely fashion, inflation could rise significantly. Incomes would also rise in that case, and the demand for housing could rise hugely. We all learned in the 1970s that real estate (and any hard asset, for that matter) is a great thing to own, especially with leverage, when inflation is rising. Today, however, both real estate and mortgage rates are priced to the expectation that inflation will remain relatively low for as far as the eye can see.

What about other inflation hedges? Gold prices are extremely high, both in nominal and real terms, and commodity prices have risen substantially. These markets arguably are priced (by speculators) to the expectation that the Fed will make a big inflationary mistake. Maybe they will, but if they don't, gold in particular could tumble much as it did in the 1980s when tight monetary policy caused inflation to fall way below everyone's expectations. It's late in the game to load up on gold, because the world has been loading up on gold for the past decade, in the expectation that inflation will rise, the dollar will collapse, and/or the global financial system will collapse. Barring any of these disasters, gold might have very limited upside but a lot of downside potential.

Treasury yields, meanwhile, are extraordinarily low, making Treasury bills, notes and bonds extraoridinarily expensive. Investors everywhere are willing to hold Treasuries at historically low levels of yield because they are very fearful of the future. With real yields on TIPS deep in negative territory, this is one more sign that expectations for future investment returns, and for real economic growth, are dismal. Thus, holding Treasuries today only makes sense if you worry about an outright depression. If the economy picks up even just a little, and/or inflation rises by even a few percentage points, Treasury yields could rise (and their prices fall) by enough to wipe out many years' worth of income.

Corporate and emerging market debt have performed very well in the past several years, because spreads to Treasuries have narrowed from very high levels and default rates have fallen thanks to an improving economy. Investment grade spreads are still somewhat wide by historic standards, but their yields have never been so low (3-3.5% currently). High quality corporate bonds still offer yields that are a few points higher than Treasuries, but if Treasury yields rise, investment grade corporate debt is going to face challenging conditions (i.e., rising yields and falling prices). In other words, current yields offer very little protection from a rising interest rate environment should the economy improve. High-yield corporate bonds offer more protection against rising yields, since their spreads to Treasuries are still relatively generous and their yields are in the range of 6-7%, but high-yield debt is no longer the slam-dunk it used to be. The current appeal of high-yield debt is that if nothing changes it offers much higher yields than Treasuries, and if yields rise, then the negative impact of rising yields would likely be offset to some degree by declining default rates and by declining spreads to Treasuries. That's because higher yields would only occur if the economy improves and/or inflation rises, and both of those conditions would make high-yield debt more attractive.

New homes sales jump 27%

New homes in September sold at a seasonally adjusted, annualized pace of 389K. That's a miserable pace of sales compared to the last 20 years, when sales averaged 770K. But the important thing to note is that sales have risen by a very impressive 27% in just the past year. That is a huge change on the margin, and it is the reason that housing starts are up 35% in the past year. The residential construction industry is realizing that the six year slump in the housing market is over; excess inventories have been worked off and new demand is materializing. This is a housing recovery, and it's still in the early stages.

Monday, October 22, 2012

The Reluctant Recovery: Part 4

This is the title of a presentation I gave October 10th to The Economic Club of Sheboygan. This post summarizes some of the key points of the presentation, and is the fourth in a series (see Part 1 here, Part 2 here, and Part 3 here.). In this fourth part, the main focus is the state of the economy. I argue that although this is the weakest recovery in generations, with a few exceptions the economy has undergone some significant adjustments and is continuing to expand, although growth is likely to continue to be rather slow and disappointing until and unless we get significant improvement in fiscal and monetary policy.

This chart is plotted with a logarithmic y-axis (as are many of my charts) in order to highlight the trend rate of growth of the economy, which for most of the past 50 years has been about 3% per year. Recessions throw the economy off track, but it usually comes back to trend after a few years. I discuss this in more detail here. This recovery, however, has been miserable. This chart suggests the economy is about 12% smaller than it otherwise could have been if the recovery were "normal." That translates to almost $2 trillion in lost output or income. This very likely the weakest recovery ever, and I think it's due to the tremendous amount of fiscal and monetary "stimulus" that has been applied in the past several years. Fiscal "stimulus" that consists of a massive increase in transfer payments only weakens growth. In the same vein, monetary "stimulus" that consists of a promise to keep rates close to zero for years, and a commitment to keep banks flush with reserves, only stimulates speculative activity while also depressing savings. In addition, it creates tremendous uncertainty about the future value of the dollar. This all combines to weaken growth because it saps the confidence and the wherewithal to make major investment decisions.

The Eurozone has taken a big hit, but industrial production there appears to be recovering in recent months, as predicted by the huge decline in Eurozone swap spreads so far this year. U.S. industrial production has been relatively stagnant this year, but there is no sign here of any collapse.

The above chart suggests that the recovery in the stock market has tracked the improvement in the underlying fundamentals of the labor market. As the pace of layoffs has dropped, equities have risen. This is my general thesis: the equity market has not been driven by rising optimism, but rather by declining pessimism. Equities have rallied reluctantly, since the economy has improved—albeit very slowly—in contrast to the very pessimistic assumptions embodied in equity prices and bond yields as I discussed in Part 1. The market's expectations, in other words, have consistently been for the economy to be in worse shape than it has actually been. The future, in other words, has turned out to be somewhat better than expected, and that is what has forced equity prices to rise, reluctantly.

The growth in jobs has been generally disappointing, but nevertheless the economy is still creating additional jobs, and there is no sign in this chart of the decline in jobs that traditionally marks a recession. We are still in the recovery phase of the business cycle, no matter how disappointing the recovery may be. With markets still braced for another recession (or worse), a continuation of modest growth should have a positive impact on equity valuations.

The chart above compares households' monthly financial payment obligations to disposable income. Thanks to rising incomes, higher savings, deleveraging, and mortgage defaults, households have significantly reduced their financial burdens in the past several years. Financial burdens today are about as low as they have been at any time in the past 40 years, in fact. Recessions are all about negative surprises and the adjustments they force. By this measure there has been a significant amount of adjustment, and that in turn lays the foundation for healthier growth in the future. All that's lacking at this point is confidence. People are still reluctant to believe that the future is bright.

The delinquency rate on credit cards and consumer loans in general has dropped considerably since the end of the recession, another sign that households are in much better financial shape these days.

In contrast to the general private sector deleveraging that has been underway in recent years, student loans are expanding at a rapid pace. This is the only category of consumer credit that has grown since the recession, in fact—consumer credit excluding student loans has actually declined by $240 billion since its peak in 2008. Student loans now account for 18% of consumer credit, whereas they were only 4% at the end of 2008. What accounts for this counterintuitive growth? The rapid growth started in early 2009, right around the time that the federal government essentially took over the student loan market. Virtually all of the increase in loans since that time has come from and is held by government agencies that have no qualms about suffering losses, since they are passed on to taxpayers. Like the housing market, which was force-fed with unaffordable loans that eventually went bust, the student loan market is a bubble in the making. The rapid growth in government-backed student loans is helping higher educational institutions to keep inflating their costs and their prices. This will likely end in tears (and defaults), with colleges and universities eventually forced to undergo the painful restructuring already experienced by the residential construction industry. The increase in student loan borrowing is not a portent of a stronger economy. There are still problems out there, and that's why everyone is reluctant to be optimistic about the future.

Auto sales are the very picture of a V-shaped recovery. Sales have increased at a 14.5% annualized pace since their recession low. Sales are still below "normal" levels, of course, but this kind of outsized growth has ripple effects throughout the economy. Sales have consistently exceeded forecasts, and this means that factories have no choice but to ramp up production and increase hiring. Real change happens when the unexpected occurs, and that is what is driving the auto industry.

Residential construction is now in the midst of a V-shaped recovery. Since early last year, housing starts have jumped by 60%, vastly exceeding virtually everyone's expectations. This also has positive ripple effects throughout the economy, and is a good sign that the housing bubble has burst. The necessary adjustments have been made (e.g., a significant decline in the inventory of new homes) to permit a return to growth. Residential construction could add as much as 1% per year to GDP growth over the next several years. It matters little that starts are still extremely low; what matters the most is the change on the margin, and that is very encouraging.

With construction rebounding, it's not surprising that housing prices are firming and even beginning to rise in many areas. The Radar Logic survey of housing prices shows they rose 5% in August compared to a year earlier. Housing today is more affordable than ever, thanks to extremely low mortgage rates and a 35% average decline in housing prices across the country in the past six years. But of course the consensus of opinion still appears to be dominated by a reluctance to believe that housing has really turned the corner—after all, there are still so many homeowners with underwatdr mortgages and so many foreclosed homes waiting to be sold. What the worriers ignore, however, is that while the supply of homes could increase, the demand for homes could increase as well, if confidence in the future were to increase.

The chart above shows that bank lending to small and medium-sized businesses is up over 22% in the past two years. Lending standards are still relatively strict, but banks are nevertheless lending more and relaxing lending standards on the margin. This is very encouraging because it reflects increased confidence on the part of both banks and businesses. Banks are more willing to lend, businesses in aggregate are more willing to borrow.

The chart above shows the fairly reliable relationship between the ISM manufacturing index and quarterly GDP growth. Manufacturing was one of the key sources of growth early in the recession, and although it is now less strong, the most recent index reading of 51.5 is still consistent with GDP growth of about 2%. The service sector version of this same index is currently at 55, and that too points to continued, albeit relatively slow, growth. Slow growth is disappointing, and there are many millions still out of work, but growing is better than not growing, and there is no sign at all in these key surveys of a recession.

Capital goods orders are a good proxy for business investment, which is the seed corn of future growth. Growth which produces rising living standards requires that we produce more with a given number of inputs. Productivity, in other words, is the source of real growth, and it requires investment in new plant and equipment, new computers, and new technology. The slowdown in business investment in recent months is disappointing, because it means growth in the future is likely to remain weak or weaken further. I think business investment has declined because of the growing uncertainty surrounding the "fiscal cliff" which is scheduled to arrive in just over two months; I don't think this is a harbinger of recession as it typically would be. Everyone knows that tax rates could soar in few months, and a drastic cut in defense spending could have negative ripple effects throughout many industries. No one knows at this point how this problem is going to be resolved; it could end up being very bad for growth or very good. This kind of binary uncertainty is likely inhibiting all sorts of decisions right now, contributing to the reluctance of investors and businessmen to embrace the equity rally and the economic recovery.

I'm optimistic that Washington and the electorate will arrive at a reasonable solution, but I can't be sure. Still, if I'm right and the markets are still braced for a recession, it's possible that even a suboptimal resolution of the fiscal cliff would fail to be unexpectedly bad news.

I'm optimistic that Washington and the electorate will arrive at a reasonable solution, but I can't be sure. Still, if I'm right and the markets are still braced for a recession, it's possible that even a suboptimal resolution of the fiscal cliff would fail to be unexpectedly bad news.

Next installment: conclusions.

Friday, October 19, 2012

Housing update

Just a few updated charts to chronicle the ongoing improvement in the housing market:

Despite all the talk about the great shadow inventory of foreclosed properties that have yet to hit the market, the inventory of homes for sale has fallen to 5.9 months' worth of sales. This is much lower than the levels that prevailed in the 1980s, and is only marginally higher than what we saw in the boom years of the early 2000s. Bloomberg's story on the subject contains these choice tidbits: "sales of previously owned U.S. homes decreased in September ... restrained by a lack of supply," and ""the median price from a year earlier jumped by the most since 2005 as inventories dwindled." If home-buying enthusiasm picks up, we could see some real shortages—and higher prices—in the coming year or two.

This last chart illustrates the degree to which prices have rebounded over the past year.

Sales are down and prices are up because of restrained supply: quite an amazing development.

Although September sales were down a bit from August levels, the above chart shows that the uptrend in sales is still intact. Sales are up 11% in the past year.

Despite all the talk about the great shadow inventory of foreclosed properties that have yet to hit the market, the inventory of homes for sale has fallen to 5.9 months' worth of sales. This is much lower than the levels that prevailed in the 1980s, and is only marginally higher than what we saw in the boom years of the early 2000s. Bloomberg's story on the subject contains these choice tidbits: "sales of previously owned U.S. homes decreased in September ... restrained by a lack of supply," and ""the median price from a year earlier jumped by the most since 2005 as inventories dwindled." If home-buying enthusiasm picks up, we could see some real shortages—and higher prices—in the coming year or two.

This last chart illustrates the degree to which prices have rebounded over the past year.

Sales are down and prices are up because of restrained supply: quite an amazing development.

Subscribe to:

Posts (Atom)