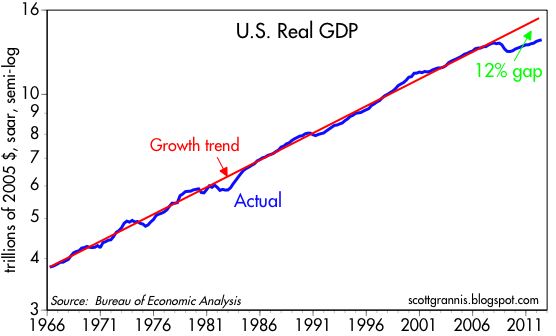

GDP was upwardly revised a bit over the past three and a half years, but as the chart above shows, the economy is still about 12% smaller than it could have been if we extrapolate from the growth trend over the past 50 years. That 12% "output gap" translates into roughly a $2 trillion shortfall in national income—that's an awful lot of money and jobs that have gone missing. This is a real national tragedy, that we have experienced such a weak recovery. If there is a silver lining to this dark cloud, it is that we now know that running up annual deficits of well over $1 trillion per year (equivalent to a whopping 9% of GDP each year on average) for the past three years hasn't managed to help the economy at all. Indeed, it's likely that the deficits are to blame for most of the underperformance, because they served mainly to redistribute income and finance a lot of wasteful and unproductive spending (e.g., Solyndra et. al.). In other words, the government spending multiplier is probably negative; we would have been much better off without all that "spending."

One other important piece of news is that despite the economy's unprecedented (in modern times) output gap, inflation remains positive, and still close to the upper bound of the Fed's target range. Keynesian theory has thus suffered a double body blow in this recovery: government spending is not necessarily stimulative, and weak growth is not necessarily deflationary.

Indeed, even as economic growth has slowed this year, from a 4.1% annualized rate in Q4/11 to 1.5% in Q2/12, forward-looking inflation expectations (as shown in the chart above, which plots the implied 5-yr, 5-yr forward inflation expectations embedded in TIPS and Treasury prices) have been rising, albeit modestly.

No comments:

Post a Comment